Stocks Rise for Another 18 months After Inversion On Average. Don't run for the hills just yet.

https://www.cnbc.com/2019/08/13/after-yield-curve-inverts-stocks-typically-have-18-months-before-doom.html

.1565716572293.png)

After a key yield curve inversion, stocks typically have another year and a half before doom strikes

KEY POINTS

- The fearsome inversion of the key 2-year and 10-year yields finally happened early Wednesday, sending markets reeling.

- Historical analysis shows that stocks typically have another 18 months to rally after an inversion, then trouble hits.

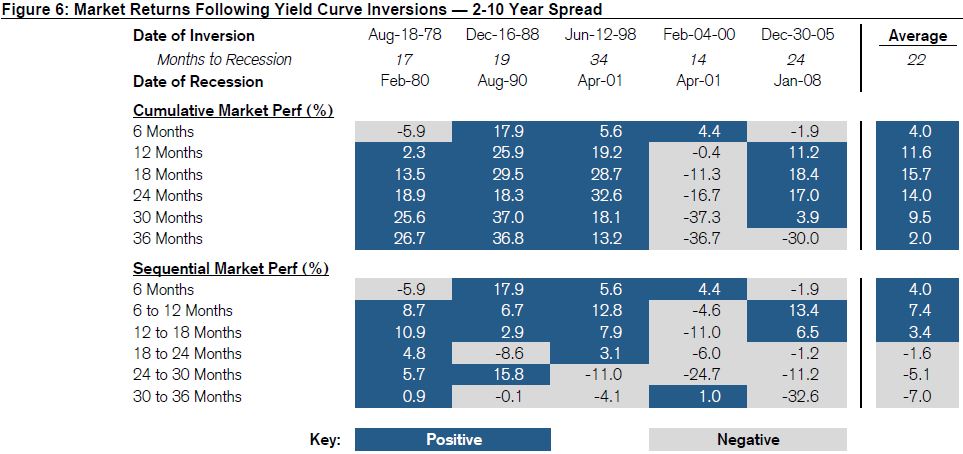

The inversion of the yield curve has been a big worry on traders’ minds all year, but historical analysis shows that stocks typically have another 18 months to rally before equity markets start to see signs of trouble.

Strategists first started publishing research on yield-curve data last summer, when a rise in short-term rates narrowed the spread between the 3-month bill rate and 10-year yield to levels not seen since the financial crisis. That part of the curve eventually inverted, but stocks continued to hit new highs.

But they’ve been waiting for the main event: An inversion of the key 2-year and 10-year yields. That occurred early Wednesday and sent stock futures reeling as traders bet this was the reliable recession indicator and the one to watch.

“While an inversion has preceded each recession over the past 50 years, the lead time is extremely inconsistent,” Jonathan Golub, chief U.S. equity strategist at Credit Suisse, wrote in July 2018. “Historically, an inverted yield curve has been accompanied by a variety of other ominous economic signals including layoffs and credit deterioration.”

Stocks typically have 18 months of gains following inversion of the 2-10 spread until returns start to turn negative, Credit Suisse data showed.

The market rallies more than 15% on average in the 18 months following the inversion. A recession hits in 22 months after the inversion, according to Credit Suisse. Sequential losses can start to add up after 18 months, Golub’s analysis showed. Yields fall as bond prices rise.

For example, the 2-10 curve first inverted ahead of the financial crisis on Dec. 30, 2005. The market posted a cumulative gain of 18.4% in the 18 months thereafter, but returned intensifying losses after 1½ years.

Echoing Golub’s analysis, Bank of America Merrill Lynch cautioned on Monday that the “S&P 500 [is] on borrowed time if the 2s10s yield curve inverts.”

“The BofAML US Economics team suggests that recession risks are rising. The 3-month T-Bill vs the 10-year T-Note curve has already inverted and the risk is that the 2s10s curve inverts as well,” BofA technical strategist Stephen Suttmeier wrote.

“Sometimes the S&P 500 peaks within two to three months of a 2s10s inversion but it can take one to two years for an S&P 500 peak after an inversion,” he added, noting that a 2-10 inversion has preceded the most recent seven recession as well as nine of the last 12.

The average and median length of time from inversion to the start of recession and 15.1 and 16.3 months, respectively, the Bank of America analysis showed.

“The typical pattern is the yield curve inverts, the S&P 500 tops sometime after the curve inverts [see above] and the US economy goes into recession six to seven months after the S&P 500 peaks,” he added.

“After the initial drawdown, the S&P 500 can have a meaningful last gasp rally.”

Comments

Post a Comment